11 mins read

Introduction

Credit risk management poses a complex challenge for global enterprises with varied geographies, currencies, and intricate corporate structures. Many credit teams are challenged with having to operate portfolios represented in many languages and, more importantly, having to navigate complicated parent-child relationships. AI-based credit scoring is emerging as a key disruptive solution in this landscape because it enables a creditor to make better-informed lending decisions. It is able to scan through extremely diversified sources of information, way beyond what is traditional, such as online transactions and behavioral patterns. This approach makes it possible for AI algorithms to uncover patterns and relationships that will remain hidden for the rest of the models, thereby ensuring an articulated and precise picture of the creditworthiness of the applicant. This article dwells on the mechanics, advantages, and practical applications of AI-driven credit scoring.

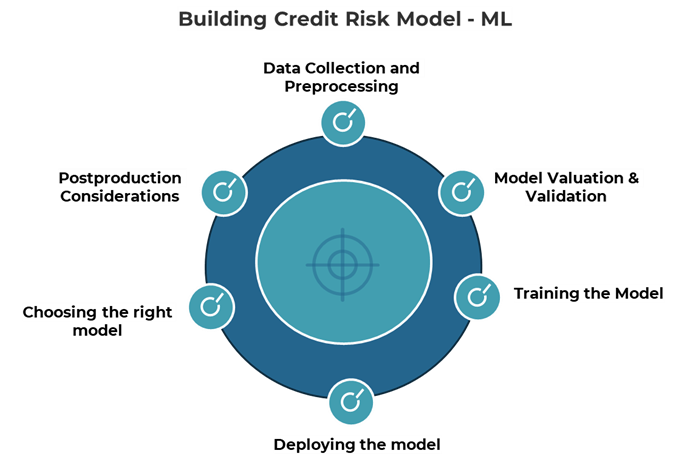

Data Collection and Preprocessing

- Data Sources:

- Historical loan performance data

- Borrower information (credit scores, income, employment history, demographics)

- Macroeconomic indicators (GDP growth, unemployment rates, interest rates)

- Alternative data (social media activity, transaction history, psychometric assessments)

- Preprocessing Techniques:

- Data cleaning to handle missing or erroneous values

- Outlier detection to identify and manage anomalies

- Normalization or standardization of features

- Encoding categorical variables (one-hot encoding, label encoding)

- Feature engineering (creation, transformation, and selection of relevant features)

Choosing the Right Machine Learning Model

- Supervised Learning Models:

- Algorithms: Logistic regression, random forests, support vector machines, gradient boosting machines

- Selection based on dataset size, complexity, and interpretability

- Unsupervised Learning Models:

- Clustering algorithms for exploratory analysis and identifying similar borrower groups

- Ensemble Methods:

- Combining multiple base models using techniques like bagging (e.g., random forests), boosting (e.g., AdaBoost, gradient boosting), and stacking

Training the Credit Risk Model

- Data Splitting:

- Dividing the dataset into training and testing sets (e.g., 70/30 or 80/20 ratios)

- Hyperparameter Tuning:

- Techniques: Grid search, random search, Bayesian optimization

- Cross-Validation:

- Techniques: Stratified k-fold cross-validation, k-fold cross-validation, leave-one-out cross-validation

Model Evaluation and Validation

- Performance Metrics:

- ROC-AUC, F1 Score, accuracy, precision, recall, confusion matrix

- Backtesting and Stress Testing:

- Assessing model performance on historical data and simulating adverse scenarios

Deployment of the Model

- Integration with Decision Systems:

- Deploying the model within existing software infrastructure

- Developing APIs for seamless integration

- Establishing governance processes for deployment and monitoring

- Real-time Scoring:

- Evaluating credit risk in real-time with efficient data processing and low-latency model inference

Post-deployment Considerations

- Monitoring Model Performance:

- Continuous monitoring for accuracy drifts and data quality issues

- Tracking KPIs such as model calibration, discrimination, and stability

- Retraining and Model Updating:

- Periodic retraining with new data and updated parameters to maintain relevance and accuracy

- Model Governance and Compliance:

- Adhering to regulatory standards, fair lending practices, and transparency

- Ensuring data privacy, security, and ethical considerations

By meticulously following these steps, financial institutions can develop robust credit risk models that enhance risk assessment and support informed lending decisions

How does it work?

It enables financial institutions to make faster and more accurate lending decisions by harnessing the advanced analytics power of AI. By transforming data into actionable insights, it streamlines the entire process of credit scoring and significantly reduces risk.

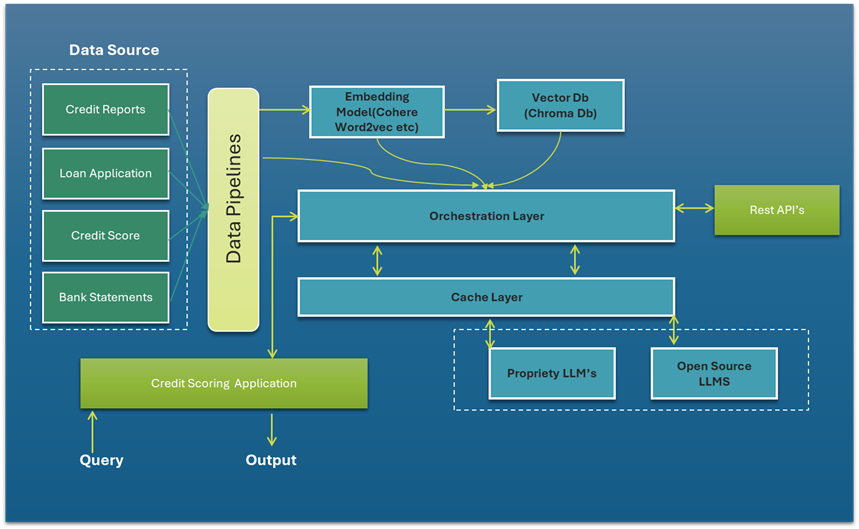

Data sources: This starts with the data collection process from all the applicable sources that relate to the whole credit scoring process. The data is inclusive of items such as:

• Credit reports, which are information availed from the credit bureaus detailing the credit history of an individual; more specifically, the payment history and outstanding debts, inquiries for credit.

• Loan applications and first-hand data from the applicants in question. These include income, employment status, and personal details.

• Bank statements: details that elaborate on how one is spending, their source of income, and the balances that are available in their accounts. All this shows the financial behavior of an individual.

• Credit scores: these are the numeric representation obtained from credit reports summarizing the credit risk of an individual based on his or her credit history.

• Behavioral Data: Social Media

Data pipelines: Information pulled in from the above channels will be processed through data pipelines. Data pipelines import, clean, and arrange the data in a way that makes it prepared for further analysis.

Embedding model: The cleaned data goes through processing with an embedding model. This model encodes textual data into vectors, which are numeric representations that can be easily understood by the AI models. This technology is powered by top models from OpenAI, Google, and Cohere.

Vector database: The generated vectors are indexed to vector databases to enable simple, fast query and retrieval processes. Key vector databases include Chroma db. and Qdrant, among others.

Orchestration layer: The orchestrating layer that would allow or deny prompt chaining, maintain flow, and support all interactions with external. The layer receives context data from vector databases and maintains memory in multiple LLM calls. What this layer will be churning out would be a prompt or sequence of prompts to be sent to an LM for processing. It is responsible for overseeing the flow of information and activities among all components in the credit scoring AI architecture..

Execution of query: The process of data collection and combination triggers as soon as the user requests some information to the credit scoring application. The requested information may be related to different areas regarding an individual’s or an organization’s credit level such as financial health, repayment capacity, risk levels, etc.

LLM processing: When the query is received, the application sends it to the orchestration layer. This layer will then extract relevant data from the vector database and the LLM cache and route it to the relevant LLM for processing. The type of query dictates the choice of LLM to use.

Output: The LLM will produce an output based on the query and the data provided to it. This output can take many forms, from financial stability summaries to the identification of risks or the generation of draft reports.

Credit Scoring App: The validated output is presented to the user through the credit scoring application. This central application brings data, analysis, and knowledge together and delivers results in a format that is appropriate for decision-makers.

Feedback loop: In this architecture, the user gives feedback on the LLM’s output. Gradually, the output attains perfection over time in terms of accuracy and relevancy, ensuring that the system never leaves any stone unturned in being state-of-the-art. Such a process also systematically gives an overall view of how AI works in improving credit scoring since it uses many sources of data and tools to get accurate and meaningful insights. But what really makes it stand out is the role that user feedback would play. This mechanism will ensure that the system keeps improving in performance and gradually becomes a live tool to score credits.

Some Use Cases

Automation of Underwriting: AI can automate the various stages involved in the underwriting process like document verification, income verification, and risk assessment, thus contributing towards quick and accurate decision-making. Customer segmentation: AI identifies customer segments with similar credit characteristics, thus allowing for targeted marketing campaigns and product offerings.

Collections optimization: AI predicts which borrowers are more likely to default and hence priorities in collections; this increases recovery. Regulatory compliance: AI assists financial institutions in checking the compliance of regulations by monitoring risks in compliance and in report generation.

Business loan approvals: AI enhances the conventional business loan approval model. The use of machine learning algorithms enables AI to scrutinize big datasets and infer results based on non-traditional and fluctuating variables, thereby conducting a more comprehensive analysis of the creditworthiness of a business. This allows for the instant assessment of adaptive learning and highly enhanced predictive ability that enables the lender to make better decisions regarding loan approval and to furnish exact terms for the loan.

Behavioural analysis examines customer spending patterns as well as consistency in payment to determine creditworthiness. For example, based on a client’s transactions, AI identifies good financial behaviour like paying bills on time and appropriate buying habits. This makes the process of credit assessment more exact in analysing the credit management skills of an individual, which ensures a better decision by the lender in granting credit and reduces their default risk.

Credit score simulation: The AI can create “what-if” scenarios regarding how borrowers would be able to impact their credit scores through specific actions, for example, paying down debt on time, amongst others. Such simulations ensure that borrowers make meaningful head or tail out of the consequences of financial decisions. The result is financial literacy and responsibility insofar as credit is concerned, because by making the right choices, therefore, this is supposed to positively impact their credit profiles.

Small business credit scoring: AI makes better judgment on credit-worthiness of small businesses by considering industry-specific data along with local economic factors. Generally, many small businesses work with a thin financial history, and it is difficult to base scoring on this foundation. This would allow the AI to consider even factors such as market trends, business models, and regional economic conditions when accessing credit worthiness at a more granular level, which will further help in the growth of small businesses and access to credit.

Top of Form

Bottom of Form

Credit scoring models.

The two general categorizations of credit scoring models include statistical and expert-based scoring models. Statistical and expert-based scoring models use different approaches to estimate a person’s credit worthiness.

Statistical scoring models: The data approach is used by the statistical scoring models in evaluating many factors derived from the credit reporting bureaus. Such factors can include the payment history, the amounts owed in loans, length of time in the credit market, types of held credit accounts, and recent credit inquiries, among others. The model correlates the factors and analyses them with some weights placed on it depending on the extent of impact on creditworthiness. The scoring process is thus thoroughly objective and not prejudice to the personal judgment and experiences of the credit officials. A credit score, therefore, by definition, is a statistical assessment of the individual credit risk based on a numerical representation of their likelihood of default-the ability to repay loans in its numerical representation.

Expert-based scoring models: expert-based scoring models are more subjective. They rely on a combination of objective financial data and subjective judgments. Other models include the individual and/or organizational financial statement, payment history, bank references, and subjective judgment of human underwriters in credit decision making. This scoring model offers more individualized judgment due to financial data that also take into consideration the context and circumstances through which a person’s credit history may have flowed.

Challenges and Considerations

The following are potential challenges and considerations that need to be addressed when implementing AI for credit modelling:

Data Quality: The quality of the data used during the training phase of an AI model will directly affect the accuracy and reliability of the model. High-quality data is paramount to achieving reliable results.

Model Explainability: AI models can be complex and hard to interpret. The understanding of how models arrive at their decisions is required for regulatory compliance and for establishing trust with customers.

Ethical Considerations: AI models have to be developed and used ethically in order not to be biased or discriminative.

Investment and Expertise: Implementing AI requires significant investment in technology, data infrastructure, and skilled personnel.

A Sample Implementation Approach

Problem: Predict the probability of default for a small business loan application.

Data: Collect data on historical loan applicants, including financial statements, credit reports, online reviews, and demographic information.

Preprocessing: Clean and preprocess data, handle missing values, and create relevant features.

Model: Build a random forest model to predict default probability based on the engineered features.

Deployment: Integrate the model into the loan origination system. When a new loan application is submitted, the model calculates the default probability. The loan officer can use this information to make a decision, along with other factors.

Monitoring: Track the model’s performance over time and retrain it periodically using updated data.

Additional Considerations

- Explainability: Ensure the model’s decisions can be understood and explained to stakeholders.

- Bias Mitigation: Address potential biases in the data and model to ensure fair lending practices.

- Privacy and Security: Protect sensitive customer data and comply with relevant regulations.

- Continuous Improvement: Iterate on the model and data to enhance accuracy and performance over time.

Conclusion

To summarize, AI is transforming credit risk management by enabling financial institutions to make smarter, data-driven decisions that boost both operational efficiency and customer satisfaction. As market circumstances change, AI provides the capabilities required to adapt, improve lending strategies, and maintain regulatory compliance, all while increasing transparency and confidence among stakeholders. To remain competitive in this marketplace, financial institutions must embrace responsible innovation, which combines technology breakthroughs with ethical concerns. This allows them to use AI’s ability to create more adaptive and trustworthy credit risk models, foresee market moves, and achieve long-term growth in an increasingly complicated financial environment.